When Tenants Go Bad: How Landlords Can Anticipate and Manage Tenant Default Risk, April 2026

A special thanks to our fantastic guests for this webinar:

- David Baxendale, Partner, Head of Insolvency, PwC

- Lawrence Fisher, Head of Strategy and Investment Analysis, NewRiver REIT (UK) Ltd

- Alberto Radice Fossati, Managing Director & Fund Manager, Realterm Europe Logistics Income Fund (RELIF)

As real estate investment returns become increasingly driven by income rather than capital growth, understanding tenant distress and managing default risk has never been more critical. This was the central message of a recent webinar hosted by Income Analytics, bringing together restructuring, retail, and logistics experts to explore how landlords and lenders can anticipate tenant failure and protect cash flows when things go wrong.

A Shift Toward Income Management

Opening the session, moderator Matthew Richardson framed the discussion against a challenging market backdrop. With limited expectations for near-term capital growth, investors are once again rediscovering “active management”: sweating cash flows, maintaining occupancy, and growing rents where possible. In this environment, tenant intelligence and early intervention are becoming decisive drivers of performance.

Understanding the Insolvency Landscape

David Baxendale, Partner in PWC’s UK restructuring practice, provided a UK-focused overview of tenant distress and insolvency processes. He outlined the wide range of outcomes that a struggling tenant may face, from solvent restructurings—such as Company Voluntary Arrangements (CVAs), restructuring plans, or schemes of arrangement—to insolvent outcomes including administration, pre-pack sales, and liquidation.

A key takeaway was that insolvency does not always mean business failure or lease termination. Many restructuring tools are designed to keep companies trading, often with compromised creditor positions. Restructuring plans, introduced during the COVID period, have become particularly powerful: courts can approve them even where some creditor classes object, including landlords.

Insolvencies: Elevated but Changing in Nature

Baxendale highlighted that UK insolvency levels have stabilised at a structurally higher level than before COVID, following the unwind of government and tax forbearance. More than three-quarters of insolvencies continue to be liquidations, particularly among micro businesses with turnover under £1 million.

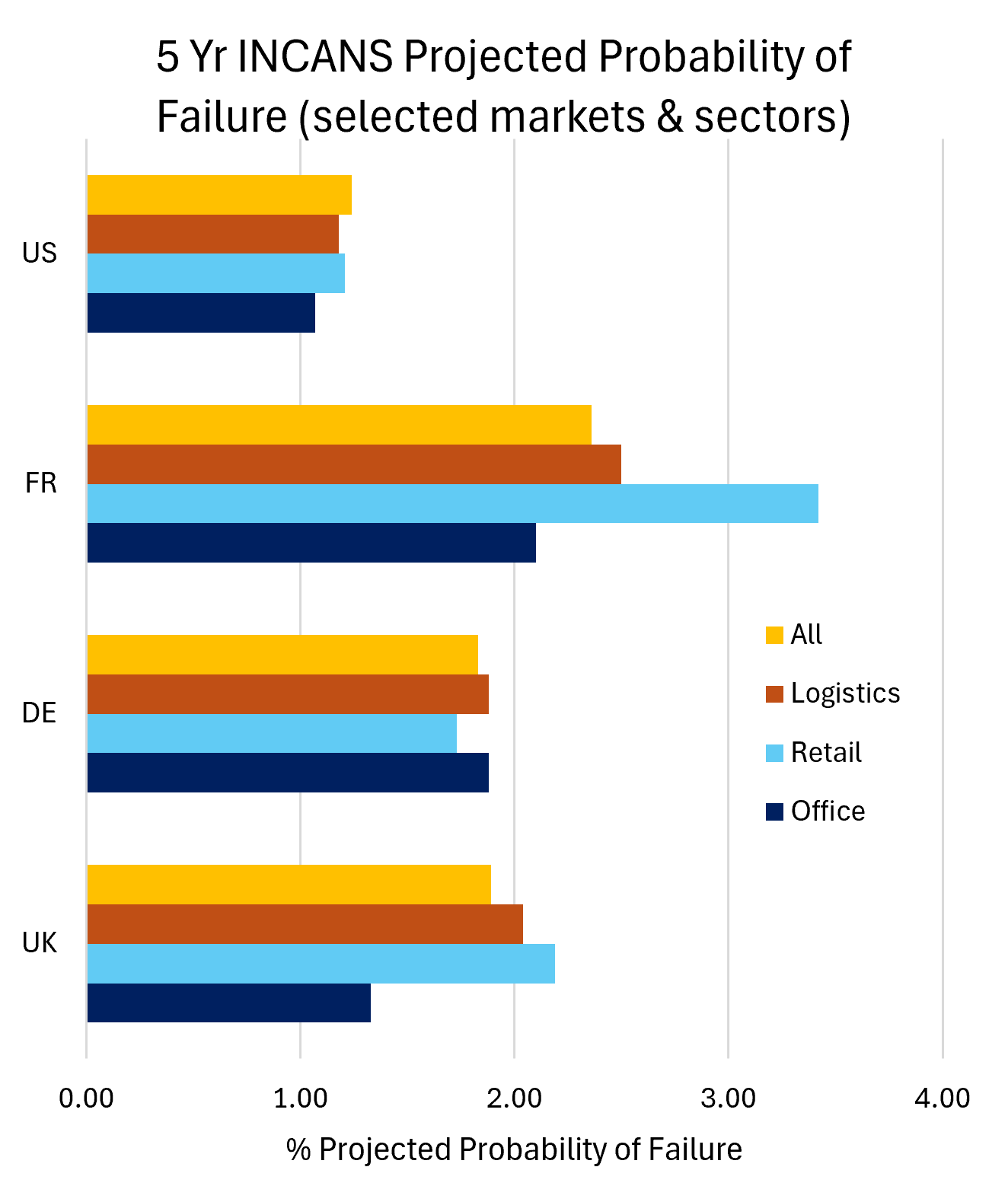

Retail, construction, wholesale, and hospitality remain the most affected sectors. In construction, thin margins and rising input costs are common drivers of distress, while retail insolvencies attract disproportionate attention because of their public visibility rather than their scale.

For landlords, this data carries an important message: risk often sits in the “tail” of smaller occupiers rather than headline exposure to large tenants.

What Landlords Can Expect in a Tenant Insolvency

From a legal perspective, landlords typically rank as unsecured creditors for unpaid rent or dilapidations. In liquidation, leases may be disclaimed and properties returned, with arrears forming unsecured claims. In administration, however, rents are payable as an ongoing expense if the premises continue to be used, and landlords retain leverage through their ownership of the asset, particularly when new operators enter under licences to occupy.

Early Warning Signs of Trouble

Baxendale emphasised the importance of spotting distress early. Red flags include management turnover, poor communication, weak governance, falling revenues, late rent payments, delayed accounts, audit issues, and negative press. While not all landlords have direct access to financial data, many of these signals are observable through public filings, market intelligence, and behavioural cues.

Retail: Worse Headlines Than Reality?

Responding from an occupier-focused landlord perspective, Lawrence Fisher of New River REIT argued that retail distress is often overstated. While well-known brands such as Poundland and River Island have restructured, many failures are retailer-specific rather than systemic. Moreover, closures often create opportunities: vacant space can be re-let quickly and at higher rents, particularly in retail parks.

New River’s approach is intensely data-driven. Real-time rent tracking, store-level spend data from banking partners, tenant credit scores, and on-the-ground intelligence from centre managers allow the firm to build detailed store P&Ls. This shifts risk assessment away from headline corporate accounts toward actual unit performance and affordability.

Active dialogue is central. By maintaining constant communication with tenants and industry bodies, problems are rarely a surprise, allowing negotiation and repositioning well ahead of formal insolvency.

Logistics and Operational Real Estate

Alberto Fossati of Realterm provided a pan-European logistics perspective, highlighting similarities with retail in the importance of active management—while noting the added complexity of operating businesses. In logistics, tenant creditworthiness is closely tied to underlying freight contracts and the mission-critical nature of locations within supply chains.

Realterm underwrites not just the tenant, but the asset’s ability to function for alternative operators. This “backfill” mindset ensures that even in tenant failure scenarios, assets can be re-let or sold, sometimes unlocking value well ahead of original expectations. Regular engagement with local managers provides intelligence that no data feed can replicate.

Planning for the Worst – and the Opportunity

Across all speakers, the conclusion was consistent: tenant failure is rarely sudden and rarely unmanageable if landlords remain proactive. Active management, diversified occupier bases, affordability discipline, and contingency planning are essential.

While tenant distress can be disruptive, commercial real estate retains a unique advantage over many asset classes: income is replaceable. Done well, defaults can become an opportunity to reset rents, improve tenant mix, and ultimately strengthen long-term income resilience.

In a market where income is king, the landlords who succeed will be those who know their tenants best—and act before problems become crises.

Thanks to all that joined us, if you missed it, please click here for a copy of the recording.